When Commodities are Plenty

Case studies in the oversupply of whiskey, pigs, and diamonds.

Whiskey

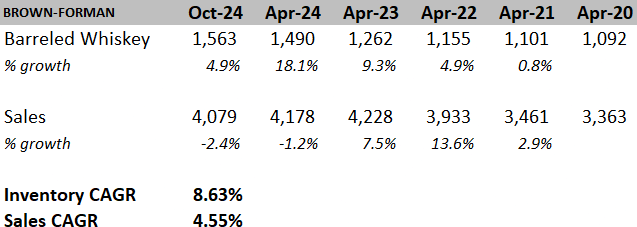

The idea for this article originated from an observation of Brown-Foreman, the producer of Jack Daniel’s whiskey and Old Forester bourbon.

Barreled whiskey production peaked in 2024 following demand growth through the COVID-19 pandemic. Isolation from quarantine created leisure time for Americans to kick back and have a cold one, and the growing prevalence of food and alcohol delivery services (eg. DoorDash and Saucey, respectively) allowed for instant gratification.

Consumers reallocated discretionary spending otherwise used at bars, restaurants, and haberdasheries to ordering in, a boon for food and drink purveyors suffering from a sudden halt in dine-in customers.

When Brown-Forman saw the uptick in demand, they barreled with haste. Sales grew 13.6% in the year following Q1 2021 and 7.5% in the year after. Following the initial sales increase, Brown-Forman increased barreling by 9%. Then, by 18% in the following year.

It’s clear to see in the graph below - the peak in inventory growth lags the peak in sales growth by two years. This makes sense considering the barreling time for whiskey; a standard Jack Daniel’s No. 7 bottle is usually aged for four years.

In the process of writing this article, the Wall Street Journal published the piece “America’s Bourbon Boom Is Over. Now the Hangover Is Here.”

The gist: whiskey producers thought demand for their products was here to stay. It isn’t.

The growing popularity of GLP-1 weight-loss drugs and cannabis use, along with a health kick from young Americans creates a dismal outlook for alcohol demand. While whiskey consumption skews toward middle-aged and older folk, alcohol is high in caloric density.

Heavy drinkers face a higher risk of obesity and are more likely to use GLP-1 drugs like Ozempic and Wegovy. Those looking to lose weight predominantly first cut alcohol consumption. But GLP-1 may also cause physiological changes associated with decreased alcohol consumption (mice are shown to cut alcohol consumption by 50% once dosed with GLP-1).

All this, on top of the U.S. Surgeon General’s claim that alcohol consumption is linked to an increased likelihood of cancer growth. Oh yeah, and that alcoholic beverages should have cancer warning labels.

Not a great omen for domestic growth in liquor consumption.

Foreign growth prospects are similarly bleak. According to the WSJ, the EU threatens to impose a 50% tariff on American whiskey in response to steel tariff claims by the soon-to-be Trump presidency.

All this raises the question: how did liquor execs play their hand so poorly? Clearly, hindsight is 20/20 (and few could’ve predicted the growing prevalence of GLP-1s), but did no one from the Brown-Forman supply chain department point out “Hey, the recent demand uptick might be a result of the American population being stuck indoors. Maybe we should hold our optimism in ramping up production”?

Pork

Pork, or more accurately the National Pork Board (a USDA-sponsored program supporting domestic pork demand) has long vied for market dominance enjoyed only by Big Chicken. Advertising campaigns have made their ambitions clear - “Pork. The other white meat.”

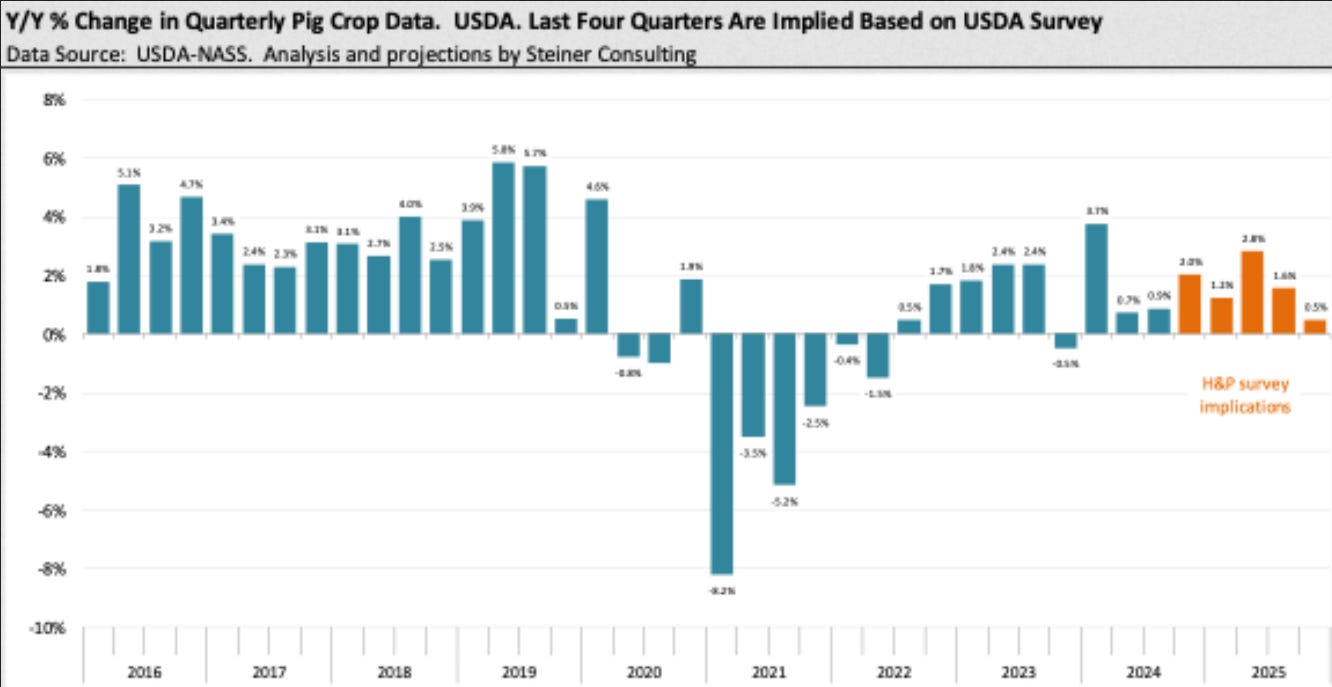

Pig farming and processing expanded from mid-2022 through 2024, motivated by an increase in foreign demand and hope for an American consumer preference shift.

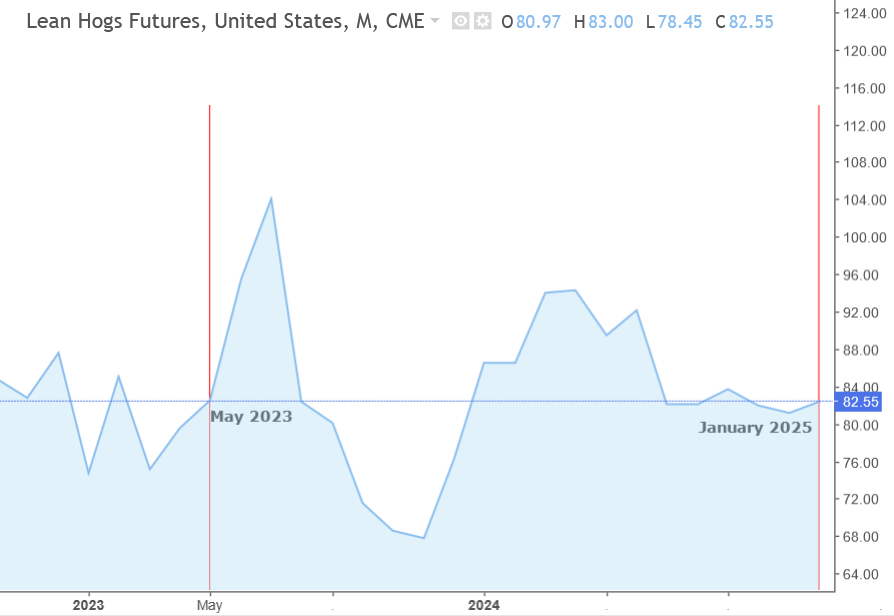

Despite supply growth, demand for pork remained largely unchanged.

Pork prices too remained unchanged in an attempt to protect the profitability of major slaughterhouses and meat suppliers.

The production of pig meat has become an increasingly costly endeavor due to new regulations around animal treatment. California’s Proposition 12 (2018) and Massachussets’ Question 3 (2016) both prohibit the confinement of sows and the sale of pork products from pigs born to confined sows.

Fewer pigs on a given tract of land equates to increased costs per pig as land maintenance costs are distributed across less animals. Prices were held constant in the face of unchanged demand, and costs were passed down to farmers.

So supply rapidly increased, while both price and demand were held (for the most part) constant.

It doesn’t take a PhD economist to predict the outcome here. In fact, let’s see what outcome ChatGPT predicts:

“The new quantity in the market increases while the price remains unchanged. This typically results in surplus supply if the price does not adjust to meet the new equilibrium.”

Diamonds

We started by looking at the whiskey market in January 2025 and moved to the mid-2023 pork market.

Now, back to the present.

De Beers is widely recognized as the largest global diamond company. In December 2024 their stockpile reached $2 billion in natural diamond inventory, a record high matched only by inventory levels after the 2008 financial crisis according to the Financial Times.

Weak demand from the Chinese consumer market along with growing US preference for lab-grown diamonds has depressed De Beers’ sales. Lab-grown diamonds are cheaper but virtually indistinguishable from their natural counterpart, aside from lacking dubious supply chains riddled with human rights abuses.

To Conclude

There’s some work to be done in long-term demand forecasting of commodities.

For now, I hold hope that I’ll soon eat pork and drink whiskey from my diamond-encrusted chalice - all on an undergraduate TA salary.